No fear-mongering here, just a reality check for the auto insurance industry.

Start with an economic theory - Creative Destruction.

Joseph Schumpeter was one of the most influential economists of the early 20th century. One of his theories included the role of creative destruction in a capitalist economy. Creative destruction refers to the continuous product and process innovation mechanism by which new production units replace outdated ones. Some consider this 'the essential fact" about capitalism.

Need proof? The compounding effect of our technological advancements is all around us and is astonishing. Businesses and industries are being transformed, digitized, or displaced at an unprecedented rate. In 1965 the companies remained in the S&P 500 Index for an average of 33 years. By 1990, that timeframe narrowed to 20 years. By 2026 the average will shrink to 14 years. Half of today's S&P companies will be replaced over the next 10 years!

Much has been said and predicted about how the future of mobility is transforming. Autonomous vehicles are on the way, no doubt. The timing we can argue, but no one will deny the trend will continue and accelerate. Most focus and public interest centers around the direct business impacts of this transformation, i.e., the Tesla's of the world vs. the legacy automakers. It will be interesting to watch and guess who will be the winners and losers of this high-stakes game for the market share of the future of our mobility.

However, what is not part of public discourse is hiding in plain sight and impacts every person that leverages a vehicle as a mode of transportation—the Auto Insurance Industry.

Depending on who is counting, the auto insurance industry is roughly 110 years old. The industry spends over $6+ Billion marketing dollars annually trying to lure and retain customers. Yet the customer loyalty is at an all-time low, with under 50% of policyholders claiming they will "definitely renew." The business model is focused on brand recognition and lowering customer acquisition costs. The reality is consumers view the service as a necessary evil, and the industry has played right along with an advertising and branding arms race. This race might be essential to compete today, but what about the industry tomorrow?

Actuarial science and risk models drive the industry and its profitability. However, the current models include imprecise data elements, and the data sources have not evolved for decades. In addition, underwriting includes controversial, and some claim biased credit and driving history along with the cost of the vehicle.

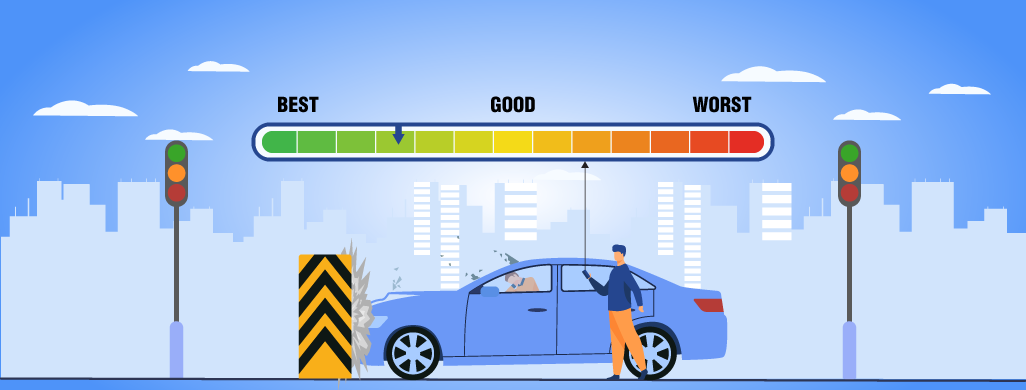

Back to the transforming auto industry, we are barreling towards autonomy. What then? Will the OEMs insure themselves? How will that impact the industry? What about for the next 20+ years when our cars are not yet fully autonomous but more "computers on wheels"? ADAS and other safety features will be taking more and more control and preventing accidents along the way. Recent studies by IIHS and HLDI have measured the dramatic real-world benefits of crash avoidance technologies. You can see the report HERE Given all this advancement and proven risk reductions, why is this information not a standard as part of the insurance process?

Thus far, the canned industry response is "while the frequency may decrease, the repair cost will go up based on the repair of sensor technology." Therefore, no change. Really? Ok, so if it is more expensive to fix, how do you "know" or validate that the car had that feature in the first place? If you can't validate it, how much are you losing to fraud without this data? It is hard to believe that these modern vehicles' intelligence and safety features are not included in the risk modeling and insurance business process. New and available data sources should shore up a clear optimization opportunity on the underwriting and claims side. It sounds like an opportunity for some carriers to jump at and differentiate to gain market share in a hurry!

In 2021 it is unbelievable that this large industry can operate in the dark. But, the good news is the data is out there. Our company has been quietly aggregating and normalizing this data for years in preparation for this transformation. Go HERE to find us. In the not-too-distant future, the entire insurance industry will leverage "vehicle build" data. Guess what? Some executives and carriers are onto this gap and opportunity and are aggressively moving forward to be in a position for the next transitionary phase of the insurance industry. Where is your company on this journey? Are you an innovator or a follower?

The modern advancements in safety features and vehicle intelligence are accelerating the need for change in the insurance industry. But, unfortunately, the reality is Insurance Carriers have not been compelled to innovate...until now. Carriers who wait too long to use new data in their models and business practices will be too late.

Perhaps spending more money on funny commercials will paper over the impending transformation?

No amount of advertisement money will change the fact that the industry must provide an optimized consumer experience at an optimized cost in a hurry. To do so, new data sources and creative destruction are a must. The customers believe the product is a necessary evil and want the TCO for their mobility to be optimized and convenient. The winners will be those who accept this reality and move aggressively toward providing this to customers.

One might look at this and think the Auto Insurance executives believe the road will go on forever and the party will never end. Joseph Schumpeter begs to differ.