If you’ve shopped for a car lately, you’ve probably noticed something: vehicle prices feel like they’re on a rollercoaster. One day, a used sedan costs more than it did new a few years ago; the next, a shiny electric vehicle’s price shifts with a sudden discount or policy tweak. It’s a confusing time for buyers, and it’s just as tricky for industries like insurance and auto lending that have long relied on vehicle prices as a steady anchor for risk assessment. Let’s explore why these prices are so unreliable these days—including some newer wrinkles like tariffs and dealer promotions—and why tying risk to them might not work as well as it once did.

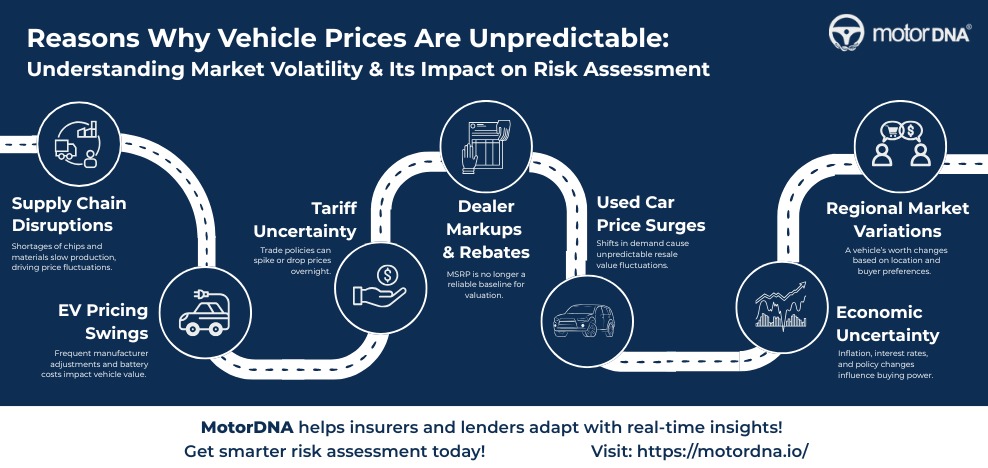

Vehicle prices used to be fairly predictable. A car’s make, model, age, and mileage gave you a solid ballpark figure, and that figure held steady enough for insurers and lenders to use it confidently. But today, things have shifted. Supply chain hiccups—like the chip shortage that started in 2020—cut new car production, pushing buyers to the used market and inflating prices. A 2022 report from Cox Automotive noted used car prices jumped 40% above pre-pandemic levels at their peak. Even now, in 2025, prices bounce around as production stabilizes but demand wavers with economic uncertainty.

The rise of electric vehicles (EVs) adds more flux. Their prices can swing wildly—think Tesla’s frequent adjustments or battery cost fluctuations. Government incentives, like the U.S.’s $7,500 EV tax credit, further blur a car’s “real” price. Tariff uncertainty piles on, too—trade policies, like a potential 25% tariff on imported cars or parts, can spike prices overnight, while a rollback might drop them just as fast.

Then there’s the tricky matter of OEM and dealer promotions. Lack of transparency here makes it hard to trust the Manufacturer’s Suggested Retail Price (MSRP). One dealership might slap on a $5,000 “market adjustment” for a hot model, while another offers a $3,000 rebate from the OEM—neither reflected in the MSRP. Actual sale prices often stray far from that baseline, varying by region, demand, or even a salesperson’s whim. Trade-ins, auctions, and regional quirks (a truck’s worth more in Texas than in New York) only muddy the waters further. It’s not that prices are chaotic—they’re just less reliable as a consistent measure than they were a decade ago.

Why This Matters for Risk Assessment

For years, insurance companies and auto lenders leaned on vehicle price as a key piece of their risk puzzle. For insurers, a car’s value helped set premiums—higher-priced cars often meant higher repair or replacement costs, so premiums reflected that. Lenders used it to gauge loan-to-value ratios, ensuring the car’s worth backed the loan amount. It made sense when prices were stable. But when a 2019 sedan’s price can double in two years—or halve if the market floods, tariffs shift, or a hidden rebate kicks in—basing risk on that number starts to feel shaky.

Take insurance as an example. If a car’s inflated price, perhaps boosted by a tariff or dealer markup, suggests a bigger payout in a total loss, premiums might climb unnecessarily. But if that price crashes later due to a policy reversal, a flood of trade-ins, or an unadvertised discount, the insurer’s risk model overestimates the real exposure. For lenders, an unstable price—say, a $30,000 MSRP car sold for $35,000 one month and $27,000 the next—complicates default scenarios. Will the car still cover the loan if repossessed? These gaps don’t mean the old methods are wrong; they just don’t fit today’s reality as neatly.

Does this mean risk assessment is broken? Not at all—it’s just time for a gentle update. Vehicle price isn’t obsolete, but it’s no longer the rock-solid indicator it once was, especially with tariffs tossing in extra uncertainty and dealer promotions clouding the picture. Thankfully, there’s a wealth of other data to lean on. For insurers, vehicle build data—like whether a car has ADAS (think automatic braking or lane warnings)—offers a clearer view of crash risk than price alone. A $20,000 car with safety tech might be less risky than a $30,000 one without it, no matter what the sale tag says. Repair cost trends, tied to specific parts like sensors or aluminum frames, also refine the picture beyond a sticker price that might not match reality.

Lenders can pivot too. Mileage, maintenance history, and even regional resale trends (tracked via VIN data) give a more reliable sense of a car’s future value than today’s volatile market price—tariffs, rebates, or markups aside. Pair that with credit profiles, and the risk assessment feels less like a guess. It’s not about throwing out the old playbook—it’s about adding new pages to it, ones that account for a world where prices can shift with a single headline or a quiet dealer deal.

Vehicle prices have always had their ups and downs, but today’s swings—fueled by supply chains, EVs, tariff uncertainty, and the hazy world of OEM and dealer promotions—are a polite reminder: they’re not the steady guide they once were. For insurance and auto lending, that’s okay—there’s better data out there to keep risk assessments fair and accurate. By looking beyond price to what a car’s made of, how it’s driven, and what it’s likely to cost down the road, we can adapt to this unpredictable market with confidence. After all, it’s not about pointing fingers at an unsteady system—it’s about finding a kinder, smarter way to move forward together.